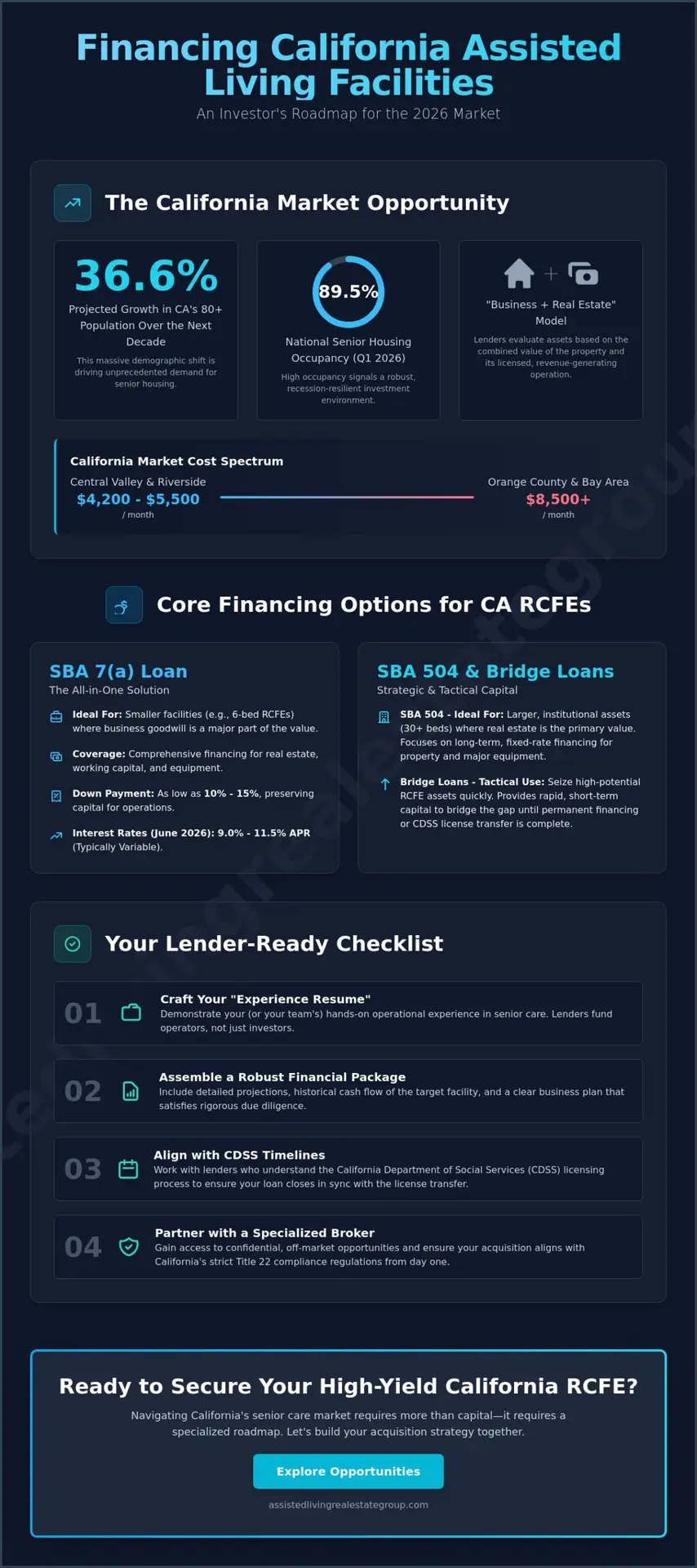

With California’s 80+ population projected to grow by 36.6% over the next decade, the demand for senior housing has reached a critical inflection point. Mastering the nuances of financing an assisted living facility purchase in California is no longer just a financial hurdle; it’s a strategic necessity for investors looking to capture this massive demographic shift. You’ve likely felt the pressure of 15% down payment requirements for special-purpose buildings or the frustration of lenders who don’t understand the intricacies of RCFE operations.

We understand that securing a high-yield asset requires more than just capital; it requires a sophisticated alignment of real estate, operations, and CDSS licensing timelines. This guide will show you exactly how to secure low-interest, long-term financing while minimizing your initial capital outlay, allowing you to bridge the gap between profit and purpose. We’ll explore current 2026 interest rates for SBA 504 and 7(a) loans, the tactical use of bridge financing, and the precise steps to ensure your loan closes in sync with your license transfer. From managing Title 22 compliance to optimizing your debt structure, you’re about to gain the roadmap needed to dominate the California senior care market.

Key Takeaways

- Understand why the hybrid “business plus real estate” model in California requires moving beyond traditional residential mortgages to specialized commercial structures.

- Navigate the strategic differences between SBA 7(a) and 504 programs to optimize your debt service when financing an assisted living facility purchase in California.

- Discover how tactical bridge financing allows you to capture high-potential RCFE assets quickly, even before permanent licensing is fully transferred.

- Prepare a lender-ready “experience resume” and financial package that satisfies the rigorous due diligence standards of California’s most active senior care lenders.

- Learn why partnering with a specialized broker ensures your acquisition remains confidential while maintaining strict alignment with California Department of Social Services (CDSS) timelines.

The 2026 Landscape of California Senior Care Financing

The 2026 investment environment for senior care in California is defined by a paradox of surging demand and constrained supply. While the 80+ population is projected to expand by 36.6% over the next decade, new construction starts remain significantly below their late 2010s peak. This supply gap pushed national senior housing occupancy to 89.5% in the first quarter of 2026, creating a robust environment for those financing an assisted living facility purchase in California. Successfully navigating this market requires a departure from standard commercial lending logic. You aren’t just purchasing a building; you’re acquiring a complex, regulated operating entity.

Lenders view these assets through a “Business + Real Estate” lens. Traditional residential mortgages don’t apply because these are “special-purpose” properties. The building’s value is inextricably linked to its licensure and ability to generate service revenue. In high-cost markets like Orange County and the San Francisco Bay Area, where monthly costs often exceed $8,500, lenders show a strong appetite for established facilities with proven cash flow. Conversely, the Central Valley and Riverside markets offer lower entry points, with costs closer to $4,200 to $5,500 per month, attracting investors focused on yield and operational turnaround. To grasp the foundational service model before diving into the debt structures, it’s helpful to review What is Assisted Living in a broader regulatory context.

RCFE vs. ARF: How Property Type Dictates Your Loan Options

Lenders categorize facilities based on their California Department of Social Services (CDSS) designation. A 6-bed Residential Care Facility for the Elderly (RCFE) is often financed through SBA 7(a) programs because the business value outweighs the real estate. However, facilities with 30+ beds are treated as institutional commercial real estate, often qualifying for SBA 504 or bridge loans. Adult Residential Facilities (ARF), which serve residents aged 18 to 59, carry distinct risk profiles. Lenders scrutinize ARF acquisitions differently, often requiring higher experience markers due to the varied care needs compared to standard RCFEs.

The Investment Thesis for California Senior Housing

Strategic professionals view California senior housing as a premier recession-resilient asset. The thesis is simple: bridge significant financial ROI with refined, compassionate care. With transaction volumes reaching $24 billion by the end of 2025, the market’s liquidity is well-established. Achieving success in financing an assisted living facility purchase in California requires more than just capital. It demands a specialized roadmap. Because these transactions are often shielded by “Confidential Marketing” strategies to protect resident stability, partnering with a niche broker is essential to accessing the most lucrative, off-market opportunities.

SBA 7(a) and 504 Loans: The Foundation of Care Facility Acquisitions

Securing a loan for a care facility isn’t like buying a standard office building. You’re financing a life-sustaining operation. For most investors, the path to financing an assisted living facility purchase in California begins with the Small Business Administration (SBA). These government-backed programs mitigate risk for lenders while offering you leverage that traditional commercial loans can’t match. In 2026, the distinction between the 7(a) and 504 programs is often the difference between a flexible start and long-term equity stability. Mastering these nuances allows you to scale your portfolio with confidence while maintaining the high standards of care the California market demands.

SBA 7(a): The All-in-One Solution

The 7(a) program is the most versatile tool in your arsenal. It’s designed to cover everything from the real estate itself to working capital and equipment. As of June 2026, variable rates for the SBA 7(a) loan program range from 9.0% to 11.5% APR. While these rates are higher than fixed-rate options, the 7(a) allows you to buy an established RCFE with as little as 10% to 15% down, depending on your experience and the facility’s cash flow. It’s the ideal choice for smaller 6-bed homes where the business goodwill represents a significant portion of the purchase price. However, the variable nature of the interest rates means you must closely monitor your debt service coverage ratio.

SBA 504: Locking in Long-Term Stability

For larger Southern California facilities, the SBA 504 is the gold standard. This program splits the loan into three parts: a first mortgage from a private bank (50%), a second mortgage through a Certified Development Company or CDC (40%), and your equity contribution (10% to 15%). In June 2026, the CDC portion offers highly attractive fixed rates, such as 5.95% for a 25-year term. This structure locks in your debt service, protecting your margins against future market volatility. Because RCFEs and ARFs are classified as “special-purpose” properties, lenders typically require a 15% down payment. This reflects the building’s limited utility for other industries.

You can often lower this initial capital outlay by utilizing the SBA Green Energy program. By implementing energy-efficient upgrades or solar installations, strategic investors can sometimes reduce their down payment requirements while increasing the facility’s net operating income. If you’re ready to explore how these structures apply to specific assets, viewing our current turnkey business acquisitions can provide a clear picture of the opportunities available in today’s market. Successfully financing an assisted living facility purchase in California requires this type of technical precision, ensuring your investment remains profitable and sustainable for the long term.

Bridge Loans and Hard Money: Tactical Capital for CA Investors

Speed is the ultimate currency in California’s competitive senior care market. While SBA products offer stability, bridge loans provide the agility required when financing an assisted living facility purchase in California. These short-term instruments allow you to bypass the lengthy 60 to 90-day underwriting cycles typical of federal programs. In 2026, California hard money rates averaged 10.05% in the first quarter, with a general range between 9.5% and 12.0%. This capital isn’t about long-term debt; it’s about seizing an opportunity before a competitor does.

Asset-based lending focuses on the property’s intrinsic value and its future potential rather than just your credit score. This is particularly relevant for distressed assets or facilities trading below replacement cost. Investors use this tactical capital to secure the real estate, then transition to permanent financing once the operation is stabilized. Your exit strategy should always be clear: bridge the gap, optimize the asset, and refinance into a low-interest SBA 504 loan once the facility meets lender seasoning requirements.

The “Fix and License” Strategy

Acquiring a non-operational facility requires a specialized approach. You can’t secure standard financing for a building that isn’t currently generating revenue. Bridge loans allow you to purchase the property and fund necessary upgrades to meet strict Title 22 safety standards. This period is critical for navigating California’s Residential Care Facilities for the Elderly (RCFE) licensing process. While you’ll manage higher interest costs during the licensing wait, the value created by transforming a vacant building into a licensed, cash-flowing asset often justifies the expense.

Speed as a Competitive Advantage

In high-demand markets like San Jose or Orange County, prime listings don’t last. A bridge loan can close in as little as 10 to 14 days, positioning your offer as “cash-equivalent” in the eyes of a seller. Bridge lenders in 2026 are increasingly sophisticated, evaluating the “business potential” of an RCFE based on regional occupancy trends, which reached 89.5% nationally this year. Expect to pay between 1 to 3 points in loan origination fees for this level of speed. This premium is the cost of entry for investors who refuse to let financing an assisted living facility purchase in California be the bottleneck that stalls their portfolio growth.

Lender Requirements: Preparing Your Application for Success

Lenders in the senior care space don’t just underwrite a building; they underwrite a reputation. When financing an assisted living facility purchase in California, your operational resume is just as critical as your balance sheet. Banks want to see a history of compassionate care and regulatory mastery. If you’re a first-time investor, you must present a detailed plan that includes a seasoned Administrator with a valid California RCFE certificate. Without this “experience factor,” securing a competitive loan becomes an uphill battle. Lenders view the operator as the primary safeguard for the asset’s value.

Financial transparency is the bedrock of a successful application. Lenders will scrutinize the last three years of Profit and Loss (P&L) statements and tax returns to ensure the business can comfortably support its debt. In the 2026 market, most California lenders look for a Debt Service Coverage Ratio (DSCR) of at least 1.25x. This means the facility’s net operating income must be 25% higher than the annual debt payments. They also account for the “Licensing Contingency,” where the loan closing must align with the California Department of Social Services (CDSS) transfer of ownership. This timing is delicate; if the license transfer stalls, the funding often follows suit.

The California Title 22 Compliance Audit

Your due diligence must extend into the facility’s regulatory history. Lenders will request the most recent Form 809 and Form 9099 reports to check for outstanding citations or recurring safety violations. They need to know the building meets current fire and life safety codes, especially given the increased enforcement seen in 2026. A specialized broker plays a vital role here, conducting rigorous due diligence for assisted living to ensure no hidden compliance issues derail the transaction at the eleventh hour.

Personal Financial Statements and Global Cash Flow

Expect a deep dive into your personal financial health. California banks prioritize “Global Cash Flow,” which looks at your income from all sources, not just the target facility. They want to see significant liquidity, often enough to cover six to 12 months of operating expenses post-closing. Common red flags include a history of Title 22 violations, occupancy trends that lag behind the 89.5% national average, or a lack of personal capital. If you want to ensure your profile meets these high standards, our confidential marketing strategy can help position your acquisition for maximum lender appeal. Successfully financing an assisted living facility purchase in California requires this level of meticulous preparation to move from curiosity to conviction.

Partnering with a Specialized California Broker

Attempting to navigate this complex market with a general commercial real estate agent is more than just a mistake; it’s a liability. Generalists often overlook the regulatory triggers that can freeze a transaction or cause a loan to be denied. In California, the sale of an RCFE or ARF is a delicate dance between real estate transfer and the California Department of Social Services (CDSS) licensing approval. A specialized broker understands that the building’s value is secondary to its operational compliance. When financing an assisted living facility purchase in California, you need a partner who can speak the language of lenders who specifically cater to this “special-purpose” niche.

The concept of “Confidential Marketing” is perhaps the most undervalued asset in a specialized broker’s toolkit. Institutional lenders require a stabilized P&L to approve funding. If a sale is made public prematurely, staff may leave and families may relocate residents, causing a sudden drop in occupancy. This volatility kills loan applications instantly. We ensure that the transition remains discreet, protecting the facility’s cash flow and your financing eligibility. By bridging the gap between sellers, buyers, and specialized lenders, we create a seamless path to ownership that general agencies simply cannot replicate.

The Turnkey Acquisition Model

Our model focuses on efficiency and certainty. We curate RCFE for sale opportunities that have already been vetted for financial viability. This means the numbers have been scrubbed to meet the 1.25x DSCR targets lenders demand in 2026. With 25 years of Southern California industry experience, we understand which banks are currently aggressive and which ones are pulling back. This insider knowledge saves you months of wasted effort and ensures your capital is deployed into high-performing assets that are ready for immediate operation.

Take Action: Secure Your Future in Senior Care

The window of opportunity in California’s senior housing sector is widening, but it requires a strategic roadmap to navigate successfully. Whether you’re looking for your first 6-bed home or a 50-bed commercial center, the right guidance is essential. Before you commit to a purchase, a confidential valuation is necessary to ensure the price aligns with the true market potential. To begin your journey, View Current California Assisted Living Listings and consult with Teri Szoke for a tailored investment strategy. Successfully financing an assisted living facility purchase in California starts with the right partner who holds the keys to this exclusive, high-barrier-to-entry market.

Capitalize on the California Senior Housing Surge

The path to scaling your portfolio in the Golden State requires more than just capital; it requires a precise alignment of debt structure, operational compliance, and licensing timelines. Success in financing an assisted living facility purchase in California hinges on your ability to meet rigorous lender standards and navigate the specific Title 22 regulatory hurdles that define this niche. We’ve explored how SBA products provide the foundation for stability while bridge financing offers the speed needed to capture high-value assets in competitive Southern California hubs.

With 25+ years of specialized experience in both RCFE and ARF regulatory environments, our team provides the seasoned expertise needed to bridge the gap between financial investment and compassionate service. We maintain an exclusive network of senior-care-friendly lenders in Southern California to ensure your acquisition is supported by the right capital partner. It’s time to transform demographic shifts into a strategic advantage for your portfolio. Consult with our RCFE Financing Experts Today to build your roadmap for success. You’re ready to achieve significant financial returns while making a tangible social impact.

Frequently Asked Questions

Can I buy an RCFE in California with only 10% down?

While a 10% down payment is possible under specific SBA 7(a) structures, most lenders require 15% for special-purpose buildings like assisted living facilities. This higher threshold reflects the property’s limited utility for other industries. If the business value significantly outweighs the real estate, some California lenders may offer more aggressive leverage, but you should prepare for a 15% equity contribution to secure the best terms.

How long does it take to get financing for an assisted living facility?

Conventional and SBA loans typically require 60 to 90 days to close in the current California market. This timeline accounts for the rigorous dual underwriting of both the real estate and the operating business. If you need to move faster to beat out competing offers in high-demand areas like Orange County, bridge financing can close in as little as 10 to 14 days.

Do lenders require me to have an RCFE Administrator Certificate?

Lenders prioritize operational expertise and almost always require the borrower or a designated manager to hold a valid California RCFE Administrator Certificate. This certification is a prerequisite for maintaining the facility’s license and ensuring Title 22 compliance. Without a qualified professional at the helm, the risk of regulatory citations makes the loan too volatile for most institutional banks and private lenders.

What is the difference between a conventional loan and an SBA loan for senior care?

SBA loans offer lower down payments and longer repayment terms but involve more rigorous federal documentation and oversight. Conventional loans usually demand a 25% to 30% down payment and higher credit scores but provide more flexibility for property management. For those financing an assisted living facility purchase in California, SBA programs are often the preferred choice to maximize leverage and preserve working capital.

Can I use a bridge loan to buy a closed care facility and reopen it?

Yes, bridge loans are the primary tactical tool for acquiring non-operational facilities that don’t yet qualify for permanent financing. You can use this capital to purchase the asset and fund renovations needed to meet strict fire and life safety codes. Once the facility is licensed by the state and stabilized with residents, you can refinance the bridge debt into a long-term, lower-interest SBA loan.

How does the California licensing process affect my loan closing date?

The loan closing is almost always contingent upon the California Department of Social Services (CDSS) approving the license transfer or issuing a Letter of Intent. This creates a delicate timing requirement where the lender and the state must move in sync. Delays at the CDSS level can push back your funding date by weeks, making it vital to have an experienced broker managing the communication between all parties.

What are the typical interest rates for RCFE financing in 2026?

In June 2026, SBA 504 fixed rates for the 25-year CDC portion are approximately 5.95%. Variable rates for SBA 7(a) programs currently fluctuate between 9.0% and 11.5% depending on the loan size and borrower profile. Hard money and bridge loans in California are trading between 9.5% and 12.0%, reflecting the short-term, asset-based nature of the capital required for quick acquisitions or facility turnarounds.

Is it possible to finance the purchase of just the business without the real estate?

You can finance a business-only acquisition using an SBA 7(a) loan or through a lease-to-own care home opportunity. This model allows you to acquire the operations and licensure of an RCFE without the massive capital outlay required for the underlying real estate. It’s a strategic entry point for professionals who want to build operational cash flow before committing to a multi-million dollar property purchase in California.