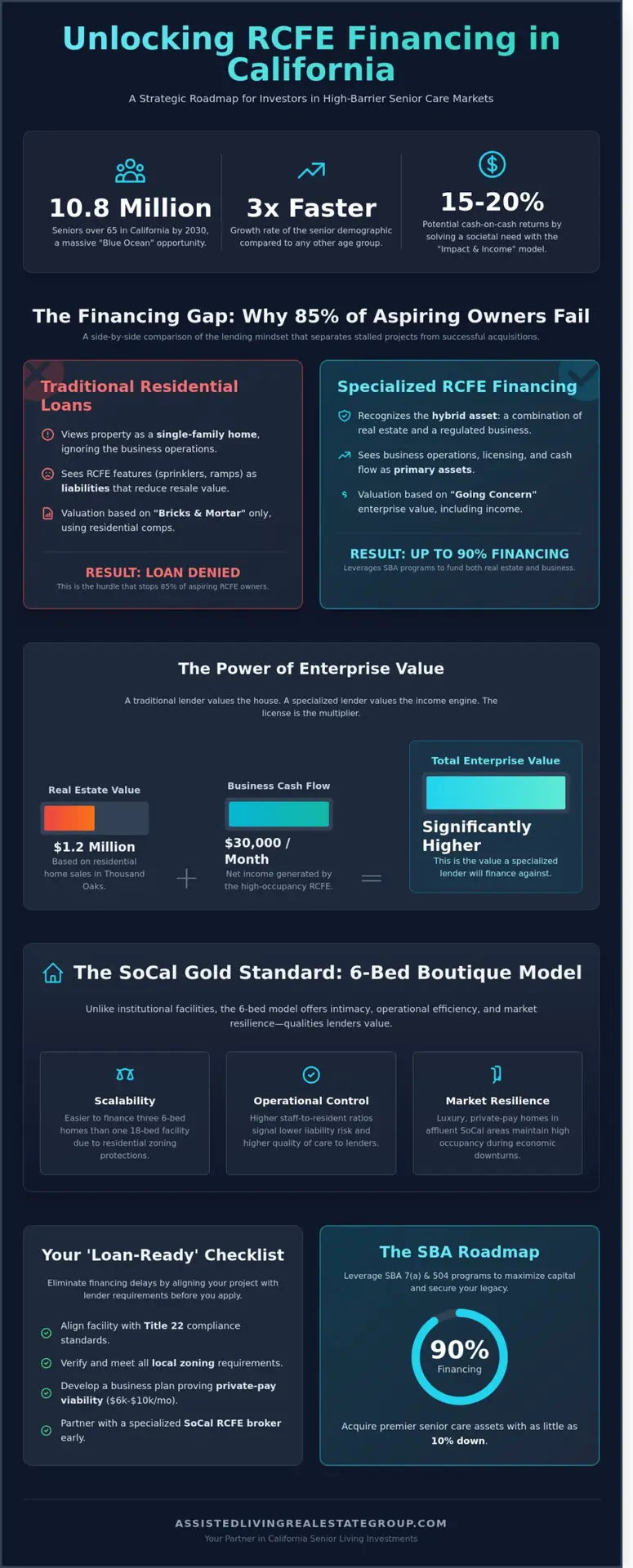

By 2030, California’s over-65 population will reach 10.8 million residents, a demographic shift that the California Department of Aging notes is growing three times faster than any other age group. This isn’t a crisis; it’s a blue ocean opportunity for investors who can solve the puzzle of rcfe financing in high-barrier markets like Orange County and Los Angeles. You’ve likely felt the sting of a residential lender rejecting your loan because they don’t understand the “Impact and Income” model of a boutique care facility. It’s a common hurdle that stops 85% of aspiring RAL owners before they even secure a property.

We agree that the gap between real estate lending and business operations is wider than it should be for such a vital service. This guide will teach you how to navigate that gap using SBA 7(a) programs to lock in 90% financing and understand the critical difference between real estate and business valuations. We’re providing the strategic roadmap to help you secure a high-occupancy asset and build a lasting legacy in California’s most lucrative senior care markets.

Key Takeaways

- Identify why standard residential mortgages fail and how specialized rcfe financing serves as the critical bridge between commercial real estate and California business acquisition.

- Discover how to leverage SBA 7(a) and 504 loan programs to acquire boutique senior care assets with as little as 10% down, maximizing your liquid capital for facility excellence.

- Explore creative capital solutions, including bridge loans and private equity, to navigate the high-barrier-to-entry market of Southern California senior living.

- Master the “Loan-Ready” checklist by aligning your facility with Title 22 compliance and local zoning requirements to eliminate financing delays before they start.

- Learn the strategic advantage of partnering with a specialized SoCal broker to protect your business value while scaling your portfolio for maximum impact and income.

Understanding the RCFE Financing Gap: Why Traditional Loans Fall Short

Securing rcfe financing requires a shift in perspective. You aren’t just buying a house; you’re acquiring a sophisticated hybrid of high-value commercial real estate and a regulated service business. In California, Residential Care Facilities for the Elderly (RCFEs) operate under the strict governance of Title 22. This regulatory oversight is exactly why standard residential mortgages are unavailable for these properties. Most traditional lenders view the presence of a care license as a disqualifying risk for a consumer loan. They see specialized fire sprinklers, exit signage, and commercial kitchens as liabilities that decrease the pool of potential residential buyers if a foreclosure occurs.

The demand for these beds is skyrocketing due to the “Silver Tsunami” hitting Southern California. By 2030, the California Department of Aging projects that 25% of the state’s population will be 60 or older. This demographic shift creates a massive blue ocean opportunity for savvy entrepreneurs. We call this the “Impact and Income” philosophy. It’s the rare ability to achieve 15% to 20% cash-on-cash returns while providing a dignified, high-quality environment for seniors who can no longer live alone. You’re solving a societal crisis while building a legacy of wealth. Many assisted living facilities fail because they lack the right capital structure from day one, making the initial funding strategy the most critical step in your journey.

The 6-Bed Boutique Model vs. Institutional Facilities

The 6-bed Residential Assisted Living (RAL) model is the gold standard for Southern California investors. Unlike massive, 100-plus bed institutional facilities that feel like hospitals, these boutique homes offer intimacy and personalized care. Financing these is unique. In cities like Thousand Oaks or Carson, zoning laws often allow 6-bed facilities to operate in residential neighborhoods without a conditional use permit. This is a massive advantage. However, lenders still scrutinize the “Boutique” luxury market differently than Medicaid-dependent sites. They want to see private-pay residents who can afford $6,000 to $10,000 monthly rates. This premium positioning justifies the higher rcfe financing costs and provides the margins necessary to weather economic shifts.

- Scalability: It’s often easier to finance three 6-bed homes than one 18-bed facility due to residential zoning protections.

- Operational Control: Smaller footprints allow for higher staff-to-resident ratios, which lenders view as a marker of lower liability risk.

- Market Resilience: Luxury boutique homes in affluent SoCal pockets maintain higher occupancy rates during downturns compared to institutional counterparts.

Real Estate Value vs. Business Enterprise Value

When you seek a loan, California RCFE lenders use a “Going Concern” appraisal. This doesn’t just look at the dirt and the walls. It evaluates the business’s ability to generate profit. Your loan-to-value (LTV) ratio won’t just depend on comparable home sales in the neighborhood. Instead, the lender analyzes your licensing status and historical occupancy rates. If a home in Thousand Oaks is worth $1.2 million as a residence but generates $30,000 in monthly net income as an RCFE, its value to a specialized lender is significantly higher. They’re financing the engine, not just the garage.

Enterprise Value Definition: In the California care home market, Enterprise Value represents the combined worth of the physical real estate and the discounted future cash flows generated by the facility’s operations and licensing.

Standard banks often miss this distinction. They might offer you a loan based on 70% of the bricks-and-mortar value. Specialized RCFE lenders, however, will often look at the total enterprise value, allowing you to leverage the business’s income to secure more capital. This is how successful investors in the California market scale their portfolios quickly. They understand that the license is the multiplier that turns a standard residential asset into a high-yield commercial enterprise.

The SBA Roadmap: 7(a) and 504 Loan Programs for CA Operators

The Small Business Administration acts as the primary engine for California’s residential care growth. For entrepreneurs eyeing the demographic shift often called the “Silver Tsunami,” SBA programs provide the leverage needed to scale. Traditional commercial lenders often demand 25% or 30% down payments. This high barrier can stall even the most compassionate visionaries. SBA options allow you to enter the market with as little as 10% down. This preserves your working capital for critical facility upgrades. You can use these retained funds to install commercial-grade bed lifts or execute ADA-compliant bathroom renovations that meet strict California Title 22 regulations.

To qualify for rcfe financing through the SBA, California operators must meet “owner-user” requirements. Your business must occupy at least 51% of the property square footage. For a boutique 6-bed facility in a residential neighborhood, this is usually a standard fit. The SBA views these facilities as active businesses rather than passive real estate investments. This distinction is what unlocks the lower down payment and longer amortization periods. It’s a strategic path for those who want to achieve both impact and income in the Golden State’s “blue ocean” of senior housing.

SBA 7(a) Loans: The Versatile Solution for Business Acquisitions

The SBA 7(a) loan program is the gold standard for first-time SoCal buyers. It’s uniquely designed to handle turnkey purchases where the value isn’t just in the dirt. In California, a facility’s “goodwill” and its hard-to-get CDSS license are major assets. Traditional banks often struggle with these “intangible assets,” but the 7(a) program embraces them. You can bundle the real estate, the business value, and even the initial working capital into a single loan. With terms extending to 25 years and interest rate caps, it provides a predictable foundation for your first boutique project.

SBA 504 Loans: Fixed-Rate Financing for Premium SoCal Real Estate

High-value markets like Van Nuys, Santa Monica, or Irvine require a more robust structure. The SBA 504 loan utilizes a 50-40-10 split. A private lender provides 50% of the cost, a Certified Development Company covers 40% through an SBA-guaranteed debenture, and you contribute 10%. This structure is ideal for those looking to acquire premium real estate with a 25-year fixed rate. It’s also an excellent tool for refinancing existing debt. By moving from a high-interest bridge loan to a 504, many operators improve their monthly cash flow by 18% or more. This stability is vital when navigating the high operational costs of California care.

Securing the right debt structure is the first step toward building a lasting legacy in senior care. If you’re ready to evaluate which program fits your specific property, you can consult with our strategic partners to map out your acquisition timeline. Success in this niche requires a blend of financial precision and a heart for service. With 10% down and a 25-year term, the math finally supports the mission.

Creative Financing: Bridge Loans, Private Equity, and Lease-to-Own

The Silver Tsunami isn’t a crisis for the prepared investor; it’s a blue ocean of opportunity. While the demand for high-quality care in California continues to skyrocket, traditional banks often hesitate to fund the very projects that meet this need. When a conventional lender says “no” because of strict debt-service coverage ratios, savvy entrepreneurs turn to private capital. In high-barrier markets like Orange County or the San Francisco Bay Area, where a 6-bed boutique facility can easily command a $2.5 million valuation, private capital provides the flexibility that institutional lenders lack. You aren’t just buying real estate; you’re investing in a specialized service model that requires a nuanced approach to rcfe financing.

Private equity is no longer reserved for 100-bed institutional facilities. We’re seeing a significant rise in private equity groups targeting Southern California’s boutique senior living sector. These investors are drawn to the “Impact and Income” philosophy, recognizing that smaller, high-end Residential Assisted Living (RAL) homes often yield higher margins than their larger counterparts. By forming a strategic partnership with a real estate investor, an experienced operator can scale their vision without being limited by their personal balance sheet. These partnerships allow you to secure prime real estate in affluent neighborhoods, ensuring your facility attracts a private-pay clientele that values intimacy and premium care.

Bridge loans serve as the essential 12 to 24-month solution for the “turnaround” facility. If you identify a distressed RCFE in a market like Riverside with a 45% occupancy rate, a standard bank will decline the loan because the current cash flow is insufficient. A bridge lender focuses on the “as-stabilized” value instead. They provide the capital to renovate the property and re-brand the operation. This short-term debt gives you the breathing room to reach a 90% census before you refinance into a permanent mortgage through the SBA 7(a) loan program, which offers more favorable long-term rates for stabilized businesses.

Lease-to-Own: The Low-Capital Entry Strategy

For many talented administrators, the biggest barrier to entry is the down payment. Lease-to-own agreements offer a powerful alternative. By securing Lease-to-Own Care Home Opportunities, you can step into an operational role immediately while building the necessary equity for a future purchase. This strategy allows you to establish a 24-month track record of Title 22 compliance and stable revenue. When you finally apply for a mortgage, your proven operational history transforms you into a low-risk borrower in the eyes of any lender.

Seller Financing and Earn-Outs in RCFE Sales

In the current California market, approximately 65% of successful RCFE transactions involve some level of seller participation. Sellers in markets like San Diego or Los Angeles often carry a second trust deed to help bridge the gap between the purchase price and the buyer’s available cash. Seller carry-back notes can bridge the gap in SBA down payments by providing the additional equity required to meet lender loan-to-value benchmarks. To protect both parties, these deals often include earn-outs. These are structured payments based on reaching specific milestones, such as maintaining a 95% occupancy rate for six consecutive months or passing a state inspection with zero deficiencies. This alignment of interests ensures a smooth transition of the legacy the seller has built while providing the buyer with a manageable path to full ownership of the rcfe financing structure.

The California ‘Loan-Ready’ Checklist: Mastering Title 22 and Zoning

California’s regulatory landscape represents the highest barrier to entry in the nation. It’s also your greatest competitive advantage. To secure rcfe financing, you must prove to the bank that you aren’t just buying real estate; you’re operating a sophisticated healthcare business. Most investors fail because they treat the bank like a mortgage broker. They don’t realize that the credit committee is looking for operational excellence, not just a high FICO score. This is your chance to show you’re a strategic partner in the senior living space.

A ‘Pending’ license from the California Department of Social Services (CDSS) often halts a loan application mid-stream. Lenders view a pending status as a 100% revenue risk. You can bridge this gap by providing a formal ‘Letter of Intent to License’ or by utilizing a bridge loan strategy that transitions into SBA 7(a) funding once the facility is active. Title 22 compliance is your secret weapon here. By presenting a binder that outlines your facility’s adherence to Title 22’s 1,500+ regulations, you demonstrate that you’re a low-risk operator who understands the ‘Impact and Income’ philosophy.

Zoning is another hurdle where local knowledge is vital. In San Jacinto, for example, facilities with 7 or more residents require a Conditional Use Permit (CUP) that can take 6 to 10 months to secure. For a 6-bed boutique RAL, California state law often preempts local zoning; however, you still need to navigate the local business license process. Securing rcfe financing in a competitive market like Carson requires a granular understanding of both state law and local municipal codes. Your business plan must articulate how you’ll manage these milestones to satisfy the bank’s underwriters.

Financial Documentation and DSCR Requirements

Lenders typically demand a Debt Service Coverage Ratio (DSCR) of at least 1.25x. For a 6-bed facility in a high-demand Southern California pocket, monthly gross revenue can hit $48,000. In contrast, a 15-bed facility might generate $125,000 monthly. You must provide three years of California tax returns and a detailed Personal Financial Statement (PFS). Banks expect to see a liquidity cushion of at least 12% of the total loan amount to cover the initial 6-month ramp-up period during the Silver Tsunami.

Local SoCal Market Analysis for Appraisers

An appraiser from Fresno won’t understand the $18,000 monthly private pay rates in Van Nuys or the luxury demand in coastal neighborhoods. You must provide ‘comps’ from other boutique RCFEs within a 3.5-mile radius. In cities like San Jacinto or Carson, highlighting the 24% projected growth of the 80+ demographic by 2028 is essential to justify your property’s valuation. This data proves your project isn’t just a house; it’s a high-yield asset in a blue ocean market.

Ready to build your legacy in the California care market? Partner with the RCFE experts to ensure your project is loan-ready from day one.

Securing Your Legacy: Partnering with a Specialized SoCal Broker

Financing a Residential Assisted Living (RAL) facility in California isn’t a standard real estate transaction. It’s a high-stakes play for a slice of the “Silver Tsunami” market. While many investors start with curiosity, reaching the closing table requires a partner who understands that a 6-bed RCFE in Orange County carries different underwriting risks than a retail strip mall. General commercial brokers often fail in this niche. They lack the nuanced understanding of Title 22 regulations and the specific EBITDA adjustments required for California facilities. This knowledge gap often leads to financing delays or outright denials from lenders who don’t grasp the boutique care model. You need a guide who speaks the language of both the lender and the caregiver.

Our group acts as the strategic bridge between your vision and the capital required to manifest it. We don’t just shop for loans; we architect the entire deal structure. By positioning your acquisition as a high-yield, mission-driven investment, we help you secure rcfe financing that reflects the true value of the business and the real estate. This specialized approach ensures that your debt service coverage ratio (DSCR) remains healthy while you scale your portfolio in the competitive Southern California landscape.

Expert Guidance from Teri Szoke and the Team

The Assisted Living Real Estate Group brings 25 years of California senior care expertise to your side of the table. We don’t just find buildings; we curate opportunities. Our team connects buyers with a vetted network of RCFE-friendly lenders across Southern California who understand the high-yield potential of this niche. If you’re ready to skip the development phase, you can explore our RCFE Sales California listings for current turnkey properties that are already primed for acquisition and immediate cash flow.

Confidentiality is the bedrock of a successful RCFE transaction. Shopping for rcfe financing without a shield of privacy is a recipe for disaster. In the tight-knit California care community, if word leaks that a facility is seeking capital for a sale, staff turnover often spikes by 18% to 22% within weeks. Families may begin looking for alternative care options, fearing a change in management will diminish the quality of life for their loved ones. We protect your business value by managing the capital search with surgical precision. We ensure that sensitive financial data only reaches vetted lenders who have a proven track record of funding California RAL projects, keeping your operations stable throughout the process.

The transition from a curious investor to a convicted owner requires more than just a bank statement. It requires a roadmap. Generalist brokers see a building; we see a legacy. We look at the cap rates through the lens of specialized care, ensuring that the “Blue Ocean” opportunity of the aging demographic is fully leveraged. This isn’t just about “doing well”; it’s about “doing good” while achieving significant financial returns in one of the most resilient asset classes in the state.

Your Next Steps in the RCFE Acquisition Journey

Success begins with a confidential valuation. You can’t secure the right leverage without knowing exactly what your target asset is worth in the current California market. We help you move from curiosity to conviction by aligning your financial “Impact and Income” goals with operational realities. It’s time to stop watching this high-growth sector from the sidelines. Contact our specialized SoCal team today to schedule your strategy session and begin your journey toward owning a boutique care facility.

Scale Your Legacy in the California Boutique Care Market

California’s aging population will reach 9 million residents by 2030, making the demand for residential assisted living a massive “blue ocean” opportunity for savvy investors. Success in this niche requires more than just capital; it demands a mastery of Title 22 compliance and a strategic approach to rcfe financing that balances SBA 7(a) leverage with private equity agility. Whether you’re targeting high-demand pockets like Thousand Oaks or expanding your footprint in Van Nuys, your ability to secure the right terms determines your ultimate ROI. You aren’t just buying property. You’re building a legacy of impact and income that serves the state’s seniors while delivering premium financial returns.

Navigating this high-barrier market alone is a risk you don’t need to take. We bring 25 years of specialized California experience and an exclusive network of RCFE-friendly lenders to the table. Our proven track record across Southern California ensures your project moves from a zoning application to a fully licensed facility with speed and precision. It’s time to turn your vision of boutique care into a tangible reality.

Secure Your RCFE Financing Strategy with Our Expert SoCal Team

The window for early-mover advantage in the SoCal boutique care sector is wide open, and we’re ready to help you lead the way.

Frequently Asked Questions

Can I get an SBA loan for an RCFE if I don’t have experience in senior care?

You can secure an SBA 7(a) loan without direct experience by hiring a licensed administrator with at least 5 years of clinical history. Lenders typically require a 15% equity injection for first-time operators in the California market. This allows you to focus on the business strategy while your team handles the daily care. You’re building a legacy of impact and income without needing a medical degree yourself.

What is the typical down payment for a boutique 6-bed RCFE in California?

Expect to provide a down payment between 10% and 25% for a boutique 6-bed facility in high-demand areas like San Diego or Los Angeles. On a $1,500,000 residential property, this equates to a $150,000 to $375,000 cash requirement. Higher down payments often unlock lower interest rates from commercial lenders. This capital ensures you have the skin in the game necessary to navigate the initial months of operation.

How does the California Title 22 license affect my ability to get financing?

California Title 22 regulations serve as the blueprint for your facility’s operational viability and your lender’s security. Banks require a detailed plan showing how your facility meets these 147 pages of strict safety and staffing requirements before they’ll release funds. Failure to comply with fire clearance or bedroom square footage mandates will halt your loan immediately. Your financing depends on your ability to prove total regulatory alignment.

Are there specific grants or loans for RCFEs in rural California areas like Fresno?

USDA Community Facilities Programs provide low-interest loans for RCFEs in California towns with populations under 20,000, including rural pockets of Fresno County. These programs offer terms up to 40 years, which significantly lowers your monthly debt service. It’s a massive opportunity to capture the rural market where competition is sparse. You can provide essential care to underserved seniors while securing a stable, long-term asset for your portfolio.

Can I use RCFE financing to renovate a residential home into a care facility?

You can use rcfe financing like the SBA 504 program to cover both the home purchase and the $100,000 to $250,000 needed for ADA-compliant renovations. This loan structure requires only 10% down, preserving your liquidity for operational reserves. Transforming a standard residence into a boutique care environment is the fastest way to create a high-value asset. It turns a simple house into a specialized, income-generating facility that serves the community.

What is the difference between financing an RCFE and an ARF in California?

RCFE financing is generally easier to obtain than ARF financing because senior care relies on private-pay residents rather than state-subsidized programs. Lenders prefer the $6,000 to $9,000 monthly rates common in California’s boutique RCFEs. Adult Residential Facilities often face tighter margins due to fixed reimbursement rates for younger adults with disabilities. Choosing the RCFE model places you in the blue ocean of the aging demographic known as the Silver Tsunami.

How long does the RCFE financing process typically take in Southern California?

The financing process in Southern California typically takes 90 to 120 days from the initial application to the close of escrow. This timeline accounts for the 30 days required for a specialized healthcare appraisal and the 45 days needed for SBA review. You should start your licensing application with the Department of Social Services simultaneously. Proactive planning ensures your doors open the moment the capital hits your bank account.

Is lease-to-own a viable option for starting an assisted living business in CA?

Lease-to-own is a strategic entry point that allows you to start your RAL business with a lower initial investment. You typically pay a non-refundable option fee of $25,000 to $50,000 while securing a 24-month window to finalize your permanent rcfe financing. This period lets you stabilize occupancy and prove your cash flow to traditional lenders. It’s a strategic move for entrepreneurs ready to scale quickly in the California market.