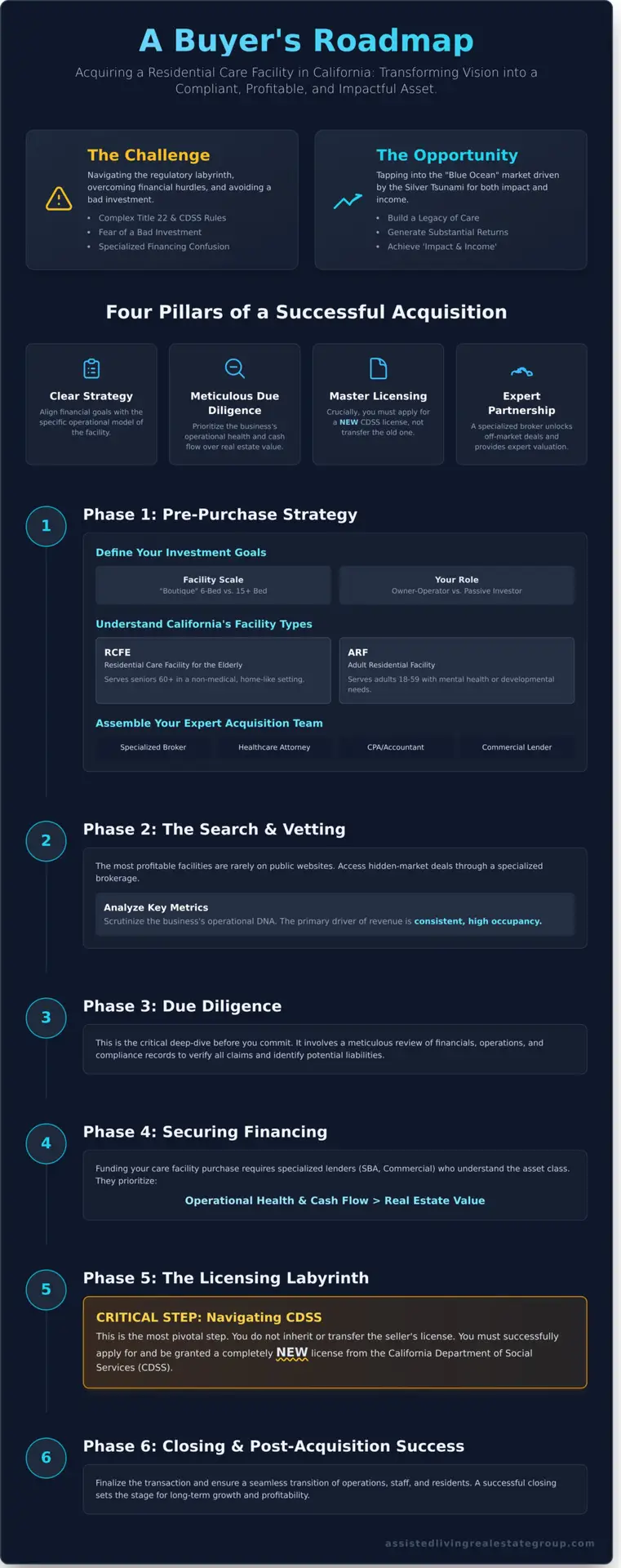

The vision is clear: generate substantial returns while building a legacy of compassionate care. Yet, for many aspiring owners, the reality of California’s regulatory landscape-a labyrinth of Title 22 and CDSS requirements-can turn that vision into a source of overwhelming anxiety. Fear of a bad investment or confusion over financing a specialized asset can paralyze even the most determined entrepreneur. That’s why mastering how to buy a residential care facility in California isn’t just about acquiring property; it’s about executing a precise strategy to secure a compliant, profitable, and impactful asset.

This definitive guide is your strategic roadmap. We demystify the entire process, from structuring the right financial deal and conducting meticulous operational due diligence to navigating the critical licensing transfer and ensuring a seamless closing. You will gain the confidence to distinguish a prime ’boutique’ care opportunity from a potential liability, empowering you to build a business that delivers both significant ‘Impact and Income’.

Key Takeaways

- A successful acquisition begins with a clear strategy, aligning your financial goals for “Impact and Income” with the specific operational model of the facility.

- Master the specialized due diligence and financing process, where lenders prioritize the business’s operational health and cash flow over the real estate value alone.

- The most critical step in learning how to buy a residential care facility in California is navigating the CDSS licensing labyrinth; you must apply for a new license, not simply transfer the old one.

- Gain a competitive advantage by partnering with a specialized broker who can unlock off-market opportunities and help you analyze the distinct values of the business versus the real estate.

Phase 1: Pre-Purchase Strategy – Laying the Foundation for Success

Before a single property is toured or an offer is made, the most critical work begins. This foundational phase is where you transform a vague ambition into a precise, actionable investment thesis. The California assisted living market represents a “blue ocean” opportunity driven by the Silver Tsunami, but navigating it requires a strategic roadmap. It starts by defining your personal “why”-your vision for creating both Impact and Income. Successful acquisition is not an accident; it is the direct result of meticulous pre-purchase planning.

Defining Your Investment Goals

Clarity is your greatest asset. Before you begin your search, you must define the exact parameters of your ideal acquisition. Are you aiming for a “boutique” 6-bed home that offers intimate, high-touch care, or a larger 15+ bed facility with greater operational scale? Will you be an owner-operator, deeply involved in the day-to-day, or a passive investor seeking strong cash flow? Establish your financial targets, including desired ROI, target cap rate, and non-negotiable cash-on-cash returns.

Understanding California’s Facility Types

A crucial first step in learning how to buy a residential care facility in California is understanding the state’s licensing landscape. The vast majority of opportunities fall under one of two categories, each serving a distinct population:

- RCFE (Residential Care Facility for the Elderly): This is the most common model, serving seniors aged 60 and over. RCFEs provide a non-medical, home-like setting offering assistance with daily living. For a foundational overview of the concept, it’s helpful to understand What is a Residential Care Facility? in its broader context.

- ARF (Adult Residential Facility): These facilities serve a younger demographic, providing care and supervision for adults aged 18-59 with mental health or developmental disabilities.

While less common in the boutique space, you may also encounter Intermediate Care Facilities (ICFs), which provide a higher level of medical care and are regulated more like skilled nursing facilities.

Assembling Your Expert Acquisition Team

This is not a solo mission. Acquiring a licensed care facility is a complex transaction with significant legal, financial, and regulatory hurdles. Attempting it without a specialized team is a recipe for costly mistakes. Your core team should include:

- A Specialized Broker: Your guide who understands the market nuances, has access to off-market deals, and can structure a winning offer.

- A Healthcare Attorney: Essential for navigating Community Care Licensing (CCL) regulations, purchase agreements, and ensuring compliance.

- A CPA/Accountant: Your expert for performing detailed financial due diligence, verifying revenue claims, and structuring the deal tax-efficiently.

- A Commercial Lender: A partner specializing in healthcare or SBA loans who understands the unique underwriting criteria for this asset class.

Phase 2: The Search – Finding and Vetting Potential Facilities

The most profitable residential care facilities are rarely found on public real estate websites. The search is a discreet, strategic process designed to uncover opportunities that deliver both impact and income. For serious investors, understanding how to buy a residential care facility in California starts with accessing these hidden-market deals.

Leveraging a Specialized Brokerage

You cannot find what is not publicly for sale. A specialized brokerage is your key to unlocking a curated pipeline of off-market, pre-vetted opportunities. Sellers in this niche demand absolute confidentiality to protect their residents, staff, and business continuity, meaning the best deals are negotiated privately. A specialist provides more than just listings; they offer expert valuation based on industry-specific metrics, ensuring you are analyzing a proven business model, not just a piece of real estate.

Analyzing a Listing: Key Metrics to Look For

Once a potential facility is identified, the real analysis begins. We guide our clients to move beyond curb appeal and scrutinize the operational DNA of the business. Focus on the numbers that truly dictate future success:

- Occupancy Rates: Consistent, high occupancy is the primary driver of revenue. Look for a stable history, not erratic peaks and valleys.

- Staffing Structure: Analyze payroll, roles, and especially employee turnover. High turnover can be a red flag for deeper operational or cultural issues.

- Financial Health: Go beyond simple profit. We analyze Seller’s Discretionary Earnings (SDE) and EBITDA to reveal the true cash flow available to a new owner-operator.

- Licensing & Compliance: A facility’s history with Community Care Licensing is paramount. A clean record is non-negotiable, and understanding the complex process for Navigating the CDSS Transfer is a critical component of your due diligence.

Real Estate vs. Business: Understanding the Deal Structure

Not all acquisitions are structured alike. The right path depends on your capital, risk tolerance, and long-term vision. The three primary models are:

- Business & Real Estate: The most common path, giving you full control over both the physical asset and the cash-flowing operation.

- Business Only (with Lease): A lower-cost entry point where you acquire the operation and lease the property, often with a future option to buy.

- Real Estate Only: A more passive investment where you purchase the property and lease it to an experienced operator, generating stable rental income.

Phase 3: Due Diligence – The Critical Deep Dive Before You Commit

Once you’ve identified a promising facility, the real work begins. This is where savvy investors separate themselves from the crowd, transforming a potential opportunity into a verified asset. The due diligence phase is your critical safeguard, an intensive investigation designed to validate the seller’s claims, uncover hidden liabilities, and confirm the true value of the investment. It starts with a signed Letter of Intent (LOI) to secure the property and grant you access, allowing you to meticulously examine the three core pillars of the business: its finances, its operations, and its legal standing.

Financial Due Diligence: Verifying the Bottom Line

A profitable care home is the foundation of both impact and income. Your first step is to move beyond the seller’s pro forma and scrutinize the raw data. This isn’t just about looking at numbers; it’s about understanding the story they tell. We guide our clients to perform a forensic-level review of:

- Financial Records: At least three years of Profit & Loss statements, tax returns, and bank records to establish trends and verify revenue.

- Resident Files: A complete audit of all resident agreements to confirm current monthly rates, care levels, and payment histories. Are the stated revenues accurate?

- Operating Expenses: A detailed analysis of vendor contracts, utility bills, and insurance policies to identify potential cost savings or upcoming price hikes.

Operational and Legal Due Diligence: Protecting Your Investment

A strong balance sheet means nothing if the operation is built on a shaky foundation. This is where you investigate the non-financial risks that can derail a new owner. A critical part of learning how to buy a residential care facility in California is understanding its compliance history. You must personally review the facility’s public file with the CA Department of Social Services, Community Care Licensing division to see all complaints and citations. This non-negotiable step reveals the facility’s true operational character. We also insist on a thorough inspection of employee files for proper certifications and a physical property assessment to identify deferred maintenance that could become a significant capital expense.

The On-Site Visit: What to Observe

Numbers and files only tell part of the story. The final piece of due diligence is feeling the pulse of the home. During your on-site visits, look beyond the surface. Observe the interactions between staff and residents-is there genuine warmth and respect? Assess the overall atmosphere. Does it feel like a vibrant community or a sterile institution? This is your chance to assess the culture you’ll be inheriting and determine if it aligns with your vision for creating a premier, boutique care environment.

Phase 4: Securing Financing – Funding Your Care Facility Purchase

Securing capital for a residential care facility is a specialized process, fundamentally different from financing a standard piece of real estate. Lenders are not just underwriting a building; they are investing in an operating healthcare business. They scrutinize the facility’s cash flow and your operational acumen as much, if not more, than the property’s physical attributes. Mastering this phase is a critical step in understanding how to buy a residential care facility in California and building a legacy of both impact and income.

Primary Financing Avenues

Navigating the capital landscape requires knowing your primary options. Each path has unique benefits and is suited for different buyer profiles and deal structures.

- SBA 7(a) and 504 Loans: These government-backed loans are the workhorse for many aspiring facility owners. They offer significant advantages, including lower down payments (often 10-20%) and longer amortization periods, which directly improves your monthly cash flow and ROI. Lenders will require a strong business plan, relevant management experience, and solid personal credit to qualify.

- Conventional Commercial Loans: For buyers with substantial liquidity, a strong personal balance sheet, or existing banking relationships, conventional loans are a viable route. Expect stricter requirements, including higher down payments (typically 25% or more) and intense focus on the facility’s historical Debt Service Coverage Ratio (DSCR) to prove profitability.

- Seller Financing: This is a powerful and strategic tool. When a seller agrees to finance a portion of the purchase price, it signals immense confidence in the business’s future success. This can bridge a funding gap and significantly strengthen your primary loan application with a bank.

Navigating these options can be complex, which is why many successful buyers partner with financial services firms that specialize in real estate loans. For instance, Icon Capital LLC offers a wide range of loan programs designed to help investors find the right capital solution for their specific acquisition goals.

Preparing Your Loan Package

Your loan package is the narrative that convinces a lender of your project’s viability. It must be professional, comprehensive, and meticulously organized. It must prove you have a clear plan for success.

Key components include:

- A Sophisticated Business Plan: This is your strategic roadmap. It must articulate your vision for providing exceptional, boutique care, detail your marketing and operational plans, and include conservative, data-backed financial projections.

- Personal Financial Statements & Resume: Lenders invest in the operator. You must present clean personal financial statements and a resume that highlights any relevant management, business, or healthcare experience.

- Seller’s Historical Financial Data: The proof is in the numbers. You will need at least three years of the seller’s profit and loss statements, business tax returns, and occupancy records to validate the asset’s historical performance.

As you compile these documents, it’s also the right time to consider your personal financial protection. Lenders, especially for SBA loans, often require key person life insurance to safeguard the loan against unforeseen events. This policy protects your family and your new business legacy. To efficiently handle this requirement, you can get instant quotes from an independent brokerage like LifeInsure.com without submitting personal contact information.

The Appraisal Process

A standard real estate appraisal is worthless in this context. The valuation of a care facility is a specialized discipline that requires an appraiser with proven healthcare industry experience. The appraiser conducts a dual analysis, determining separate values for the tangible asset (the real estate) and the intangible business enterprise (the license, goodwill, and cash flow). The final loan amount a bank will offer is directly tied to this comprehensive valuation, making the choice of a qualified appraiser a crucial factor in the process of how to buy a residential care facility in California.

Phase 5: The Licensing Labyrinth – Navigating the CDSS Transfer

You’ve navigated due diligence and secured financing. Now comes the most critical barrier to entry, the step that transforms a savvy investor into a licensed operator: the California Department of Social Services (CDSS) licensing process. For many, this is the most daunting part of the acquisition journey. The single most important concept to grasp is that you are applying for a brand-new facility license; you are not simply transferring the seller’s.

Successfully timing your application submission to coincide with the close of escrow is a strategic art, one that separates a smooth transition from a costly, delayed one. This is where meticulous preparation meets expert execution.

The Initial License Application (LIC 200)

Your journey begins with the comprehensive Initial License Application, form LIC 200. Precision here is non-negotiable, as even minor errors can trigger significant delays. You will need to assemble a complete package that includes:

- Detailed financial verification to prove solvency and operational capital.

- Personal references and background checks for all principals.

- Proof that you are a certified RCFE Administrator or have hired a qualified professional to fill the role.

The CDSS Review and Facility Inspection

Once submitted, your application is assigned to a Licensing Program Analyst (LPA). This individual is your primary state contact who will scrutinize your submission and conduct the pre-licensing facility inspection. To prepare, you must ensure the physical plant is in perfect compliance. Common issues that stall applications include improper grab bar placement, missing fire extinguishers, or incomplete resident files. Proactive preparation for this visit is paramount to your success.

Coordinating with the Seller for a Smooth Handover

A seamless transition hinges on deep collaboration with the seller. This is a vital part of learning how to buy a residential care facility in California while upholding the highest standards of care. Your primary goal is ensuring absolute continuity of care for residents, with no disruption to their quality of life. Work directly with the seller to address any pre-existing deficiencies, ensuring the home meets all state standards on day one of your ownership. This complex coordination is where expert guidance becomes invaluable.

Don’t navigate this intricate process alone. Let our experts guide you through the licensing maze. Contact us today.

Phase 6: Closing the Deal and Ensuring Post-Acquisition Success

You’ve navigated the complexities of due diligence and secured financing. Now, you stand at the threshold of ownership. This final phase is not an endpoint; it is the beginning of your legacy. The day you receive the keys is the day your vision for creating a premier boutique care environment-and a powerful financial asset-truly begins.

The Escrow and Closing Process

The final stage of how to buy a residential care facility in California involves a precise coordination of legal, financial, and regulatory milestones. This is where your team’s expertise becomes critical to ensure a seamless transfer of ownership. Key actions include:

- Finalizing Documents: Working with your lender to execute final loan documents and coordinate the transfer of funds through escrow.

- Executing the Purchase Agreement: Signing the final purchase agreement and all ancillary legal documents, officially transferring the business and real estate assets.

- Securing Your License: Receiving your official Residential Care Facility for the Elderly (RCFE) license from the California Department of Social Services (CDSS), a monumental step that permits you to operate.

Your First 90 Days as the New Owner

A successful transition is paramount for retaining the two most valuable assets you’ve just acquired: your staff and your residents. Your initial actions will set the tone for your entire ownership. Focus on communicating your vision with clarity and compassion, meeting with residents and their families to build trust, and methodically implementing the operational improvements you identified during your analysis. This is your opportunity to demonstrate leadership that values both quality of life and operational excellence.

Long-Term Strategy for Growth

True success in this industry is about building a sustainable model of Impact and Income. Your long-term strategy must be geared toward growth and optimization. This includes deploying a sophisticated marketing plan to maintain high occupancy, investing in professional development to cultivate a loyal and highly-skilled team, and strategically planning for future expansion. Whether it’s acquiring another facility or enhancing your current property, your vision should always be scaling your positive impact and your financial returns. Navigating this ongoing journey from owner to industry leader requires a dedicated partner. To continue building your portfolio, explore the opportunities with Assisted Living Real Estate Group.

Your Blueprint for Success in California’s Care Market

Acquiring a residential care facility is more than a transaction; it’s the creation of a legacy. As this guide has detailed, mastering how to buy a residential care facility in California demands a meticulous pre-purchase strategy, an exhaustive due diligence process, and a clear-eyed approach to the state’s complex licensing labyrinth. The path is complex, but you don’t have to walk it alone.

With over 25 years of specialized experience in RCFE and ARF transactions, The Assisted Living Real Estate Group is the strategic partner that turns complexity into clarity. We provide expert guidance through every critical phase, from initial valuation to final licensing, ensuring your investment is both sound and successful. Our confidential marketing protects sellers while connecting qualified buyers like you to premier, often off-market, opportunities.

Your opportunity to achieve both impact and income is here. Take the definitive next step in your investment journey. View our current listings of premier California care facilities for sale and begin building a legacy of compassionate care and financial success today.

Frequently Asked Questions About Buying a Care Home in California

How long does it typically take to buy a residential care facility in California?

The acquisition timeline typically ranges from 4 to 9 months. This includes 1-3 months for identifying a property, conducting due diligence, and securing financing. The most significant variable is the Community Care Licensing Division (CCLD) application process, which can take an additional 3-6 months post-escrow. A strategic, well-managed approach is essential to navigate these milestones efficiently and avoid costly delays in this high-opportunity market.

Do I need to be a licensed RCFE Administrator to buy a facility?

No, you do not personally need to be licensed to own the facility. The owner’s role is that of an investor and asset manager. However, California law mandates that every licensed Residential Care Facility for the Elderly (RCFE) must have a designated, certified Administrator to manage daily operations and resident care. This allows you to focus on the business’s financial performance while entrusting operational excellence to a qualified professional.

What is the average cost or price range for a 6-bed care facility in California?

The price for a boutique 6-bed Residential Assisted Living (RAL) home varies dramatically by location, from approximately $750,000 in inland areas to over $2 million in prime coastal markets. This valuation includes both the real estate asset and the business value, which reflects existing cash flow and goodwill. A thorough analysis of both components is critical to ensure you are securing a high-performance asset poised for significant ROI.

How much of a down payment is required to finance an assisted living facility?

Investors should prepare for a down payment between 15-25% of the total purchase price. Financing options like the SBA 7(a) or 504 loan programs often allow for down payments on the lower end of this spectrum, typically 15-20%. In contrast, conventional commercial lenders may require 25% or more. This initial capital is the key to unlocking an asset class that delivers powerful cash flow and builds a lasting legacy.

What are the biggest risks or mistakes to avoid when buying a care home?

The most critical mistake is performing inadequate due diligence, particularly on the facility’s licensing and compliance history with the CCLD. Overlooking past citations can signal deep operational issues. Another common pitfall is underestimating the working capital required for the first six months. A successful acquisition demands a forensic review of financials and a solid operational plan to ensure a seamless transition and protect your investment from day one.

Can I buy a facility if I don’t have direct experience in healthcare?

Absolutely. Many of the most successful owners are sharp investors, not clinicians. The strategy is to acquire the asset and build an expert operational team. Your role is the visionary and investor; you hire a licensed administrator and skilled caregivers to provide exceptional boutique care. Understanding this model is fundamental to learning how to buy a residential care facility in California and build a portfolio that generates both “Impact and Income.”